We previously talked about things to avoid before applying for a mortgage, now let’s talk about what not to do after. So you’ve just applied for a mortgage, and now you’re in that waiting game and there are a few things you wanna steer clear of during this time to keep things smooth sailing. Below is a useful infographic from the folks at Keeping Current Matters to show just that.

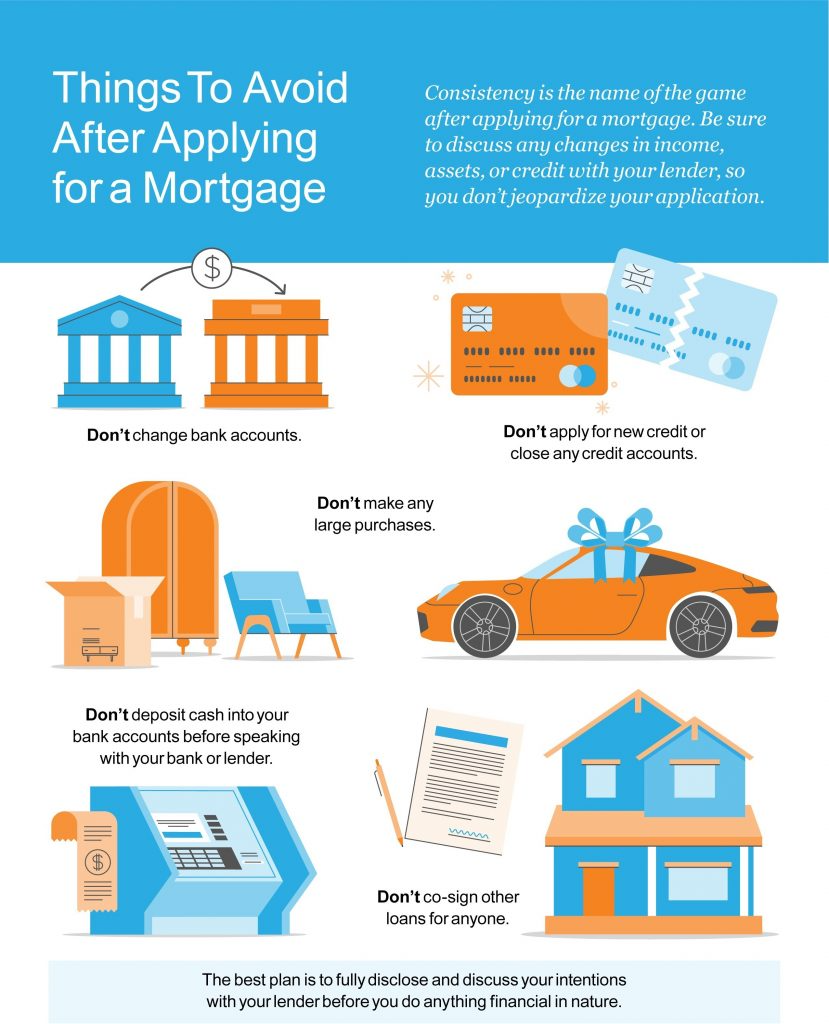

Things to Avoid After Applying for a Mortgage

Don’t change bank accounts.

Doing this would mess up the lender’s ability to verify your financial history and might slow down or complicate your loan approval. Also, try to avoid switching jobs or making any major career moves if you can help it. Keep things as is during the approval process to make the process smoother and faster for everyone involved.

Don’t apply for new credit or close any credit accounts.

Hold off any plans to apply for new credit card or close any credit accounts as it can change your credit score and debt-to-income ratio, which might jeopardize your mortgage approval. If you ready have to, wait until after your mortgage is finalized before making any credit changes.

Don’t make any large purchases.

It mght be tempting, right? Going on a shopping spree right after applying for a mortgage can increase your debt and alter your credit score, potentially messing up your loan approval. Big expenses like buying a new car or a booking a vacation can make lenders doubt your financial stability. Keep your spending in check until your mortgage is finalized to avoid any hiccups.

Don’t deposit cash into your bank accounts before speaking with your bank or lender.

When you’re in the middle of the mortgage process, suddenly depositing a lot of cash into your bank account can raise red flags for lenders. They might get curious about where the money came from, and it could slow down your approval. Stay clear and consistent and always check in with your lender before making any big moves with your money.

Don’t co-sign other loans for anyone.

When you co-sign for someone else’s loan after applying for a mortgage, it can mess with your debt-to-income ratio, making you look riskier to lenders. This might affect your mortgage approval or the terms you get. It’s best to hold off on co-signing until after your mortgage is settled to avoid any complications.

Bottomline, lenders like to see stability so keep things steady until you’ve got those keys in hand! If you’re all set and interested in being qualified to purchase a home right now, please feel free to contact the agents at Broadpoint Properties.