So you’re ready to dive into the world of homeownership and get a handle on the financial side of things? One of the first things you’ll want to figure out is how much house you can actually afford. Let’s break it down.

Image from Smart Asset

According to Smart Asset’s estime, to afford a home in San Diego, you need to have a minimum annual income of $75k to afford a $460k home after paying a 20% down. Smart Asset has a helpful tool to help you get an estimate how much home you can afford according to your salary. Check it out here: https://smartasset.com/mortgage/how-much-house-can-i-afford. But note that this is a quick look up if you’re curious — it’s still best to reach out to a mortgage professional and get pre-approved.

There are several factors to consider for you to know how much home you can afford namely your salary, debt, credit score and the actual costs of buying a home. There are a couple of rule of thumbs that are widely used in real estate:

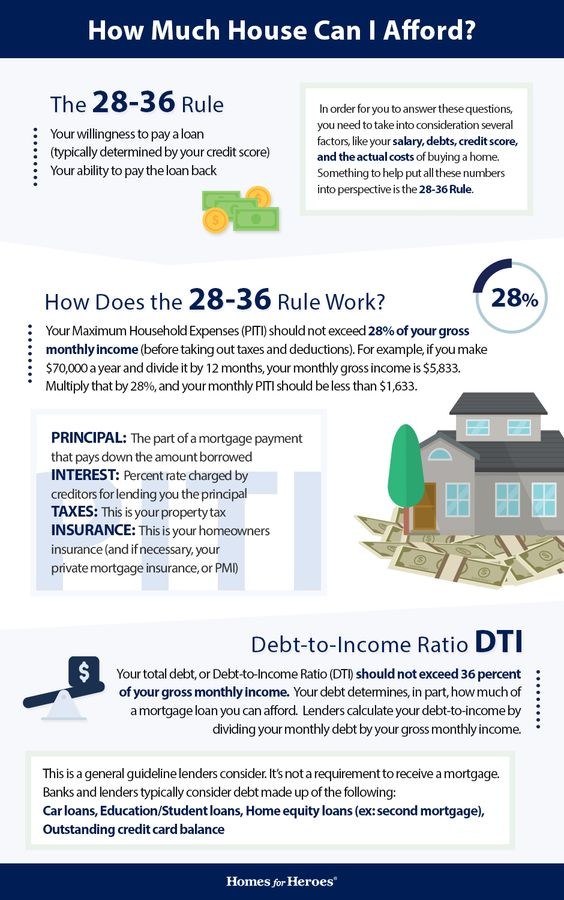

The 28-36 Rule

Basically, it’s a rule of thumb that lenders use to help determine how much house you can afford without overstretching your finances.

The 28 part means that ideally, your total housing costs shouldn’t be more than 28% of your gross monthly income. That includes things like your mortgage payment, property taxes, HOA dues and homeowner’s insurance.

And then there’s the 36 part, which says that your total debt payments—including your housing costs—shouldn’t exceed 36% of your gross monthly income. That means factoring in things like car loans, credit card payments, and any other debts you might have.

Let’s break it down with an example.

Let’s say your gross monthly income (before taxes) is $5,000.

According to the 28-36 rule:

28% Rule: Your housing costs shouldn’t exceed 28% of your gross monthly income.

$5,000 * 0.28 = $1,400

So ideally, your total housing costs, including mortgage, property taxes, and insurance, should not be more than $1,400 per month.

36% Rule: Your total debt payments, including housing costs, shouldn’t exceed 36% of your gross monthly income.

$5,000 * 0.36 = $1,800

This means that all your monthly debt payments, including housing costs, should not be more than $1,800.

It’s not set in stone, but it’s a good starting point to make sure you’re not biting off more house than you can chew.

Debt-To-Income (DTI) Ratio

Essentially, it’s the ratio of your monthly debt payments to your monthly gross income. The standard DTI ratio that lenders often use is 43%. That means your total monthly debt payments shouldn’t exceed 43% of your gross monthly income.

To get a quick idea of where you stand, you can use an online calculator to crunch the numbers. But for a more accurate assessment, it’s always a good idea to chat with a lender. They can give you personalized advice and help you navigate the mortgage process with confidence!

Image from Homes for Heroes

By carefully assessing your salary, financial situation, and housing needs, you can confidently know how much housing you can afford. Remember to prioritize financial stability and avoid stretching yourself too thin to have a stress-free and enjoyable home buying experience.

And if you’re looking for the best lenders and real estate agents in San Diego, feel free to reach out to our team for recommendations. Property owners who need help managing a rental can also explore our San Diego property management services for support with tenants, maintenance, and day-to-day operations.