VA loan questions are some of the ones we get asked most often. Our active-duty military and honorably discharged veterans have some really great possibilities available for them in the real estate space, and there are some lesser-known facts about how to take advantage of these special perks! We are setting the facts straight — we are debunking some of the most common misconceptions about VA home loans so you can avoid mistakes and bad decisions during the home buying process.

Eliminate VA Home Loan Confusion

Confusion #1:

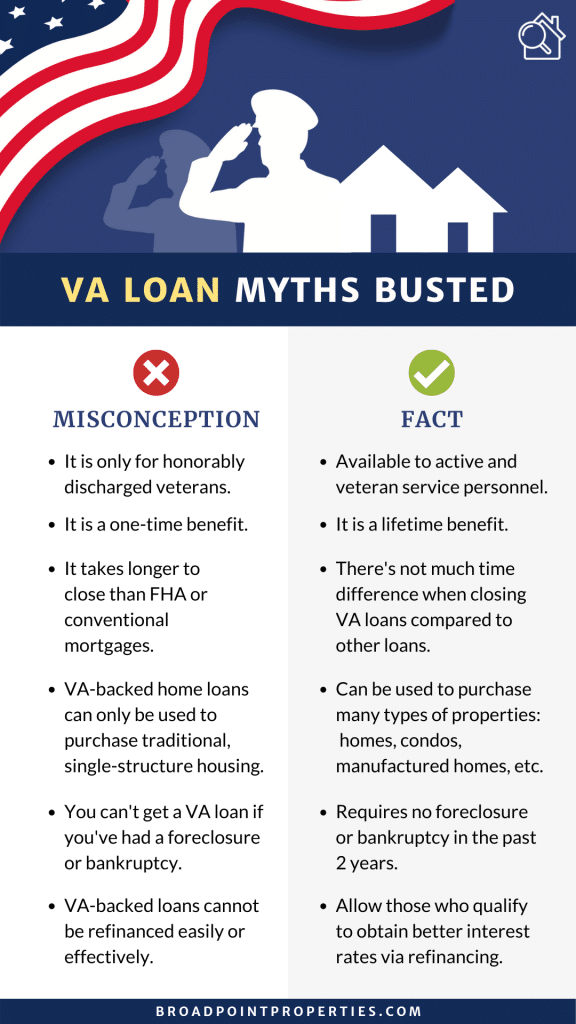

VA loans are only for honorably discharged veterans.

Fact:

Active-service members, veterans, and eligible surviving spouses can make use of this benefit.

Confusion #2:

You can use this only once.

Fact:

Veterans affairs members can enjoy this lifetime benefit. Qualified Veterans can use the VA Loan Guaranty Program over and over again. In fact, it’s possible to have more than one active VA Loan at the same time. Even losing a VA Loan to foreclosure doesn’t mean you’re no longer eligible.

Confusion #3:

It takes way longer to close than FHA or conventional mortgages.

Fact:

There is really not much difference in how long VA loans are closed compared to other loans. According to Ellie Mae’s January 2021 Origination Report, it took an average of 66 days for a VA loan to close – from applying for a mortgage to getting the keys to the home, compared to a conventional loan’s average of 57 days.

Confusion #4:

VA-backed home loans can only be used to purchase traditional, single-structure housing.

Fact:

VA home loans can be used to purchase many types of properties: homes, condos, manufactured homes located in the United States, its territories, or possessions (Puerto Rico, Guam, Virgin Islands, American Samoa, and Northern Mariana Islands). It cannot be used to purchase a cooperatively owned apartment, farm, vacant land, investment property, or business loan.

Confusion #5:

You can’t get a VA loan if you’ve had a foreclosure or bankruptcy.

Fact:

VA Loans also allow Veterans and active military to bounce back faster after a bankruptcy, foreclosure, or short sale. An applicant must not have had any foreclosure or bankruptcy in the past 2 years.

Confusion #6:

VA-backed loans cannot be refinanced easily or effectively.

Fact:

There is actually a 6% rise in the number of people availing of VA loans from last year. Veterans who have an existing VA-backed home loan and want to reduce their monthly mortgage payments or make payments more stable can take advantage of Interest Rate Reduction Refinance Loan (IRRRL).

Often active-duty military and veterans do not know that they have some of the best home buying benefits available! So if you or anyone you know can make use of the information above, feel free to share this.